Brandon Wilson, Sales and Service Engineer at Edge Technologies, has expanded his territory to include Michigan while continuing to serve Eastern Canada. Wilson succeeds Regional Sales Manager Carl Miller and brings over 20 years of experience in machining and manufacturing.

Solar Atmospheres' new 28,000-square-foot facility in Berlin, Connecticut is progressing on schedule for a fourth-quarter 2026 opening. Vacuum furnaces have been installed and office areas are nearing completion at the Spruce Brook Industrial Park location, which will expand the company's vacuum heat treating capabilities throughout the Northeast.

The NSSF-adjusted NICS figure for July 2026 reached 1,061,883, an 8.5 percent increase from July 2025's 978,731. NFA checks surged 108.8 percent to 130,013, with Texas, Florida, and Virginia leading in NFA activity. Texas topped adjusted NICS checks among all states.

Solar Atmospheres has installed an 11,000-gallon stainless steel recirculating water quench tank for its state-of-the-art titanium drop bottom furnace, scheduled for full commissioning by September 2026. The furnace will solution treat titanium bars, forgings, and large components for aerospace, defense, and industrial applications.

NSSF praises the Trump administration's new rules transferring firearm suppressor export licensing from the State Department to the Commerce Department. Lawrence G. Keane, NSSF Senior Vice President & General Counsel, stated the reforms will enable American suppressor manufacturers to compete more effectively in overseas markets without burdensome regulatory requirements.

AustriAlpin Inc. now fulfills U.S. orders from its North Carolina warehouse, eliminating tariff fees and reducing shipping costs. The company introduced new 1.5-inch COBRA Fashion buckles and expanded 2-inch COBRA buckle options for manufacturers and retailers.

Payroc, an official NSSF Affinity Partner, launched Roc Terminal+, an all-in-one smart payment terminal designed for firearms retailers. The device offers portable payment acceptance, omnicommerce capabilities, inventory management, and QuickBooks integration, backed by Payroc's firearms-friendly processing expertise.

Range Tool Company LLC, a northern Minnesota AR-15 component manufacturer celebrating 15 years, announced its expanded presence at SHOT Show 2027, including its debut on the Main Show Floor alongside booths in the Supplier Showcase and Supplier Showcase Reloaded to connect with dealers and industry partners.

HERMLE will showcase five machines at IMTS 2026 in Chicago, including the C 62 U MT, its largest machine ever displayed in North America, and the debut of the new C 22 U MT 5-axis mill-turn platform. The display represents HERMLE's largest presence at a North American trade show, featuring automated production cells and Metal Power Application additive manufacturing technology.

Check-Mate, a leading American firearm magazine manufacturer, announced its sponsorship of World Champion pistol shooter Jessie Harrison. Harrison, the first woman to earn Grand Master status in USPSA, will compete using Check-Mate magazines while representing the company's commitment to quality and reliability.

It’s that time again. How much of item 12345 do I need to buy? I purchased 100 units the last two months, but demand seems to have increased a little, almost 10%, and inventory is lower than it usually is, so maybe I’ll buy 110 this time? Is this your buying process? Ugh!

I apologize right now that I’m an engineer and very number driven, especially when it comes to procurement (buying) and inventory management. As background, I’ve rebuilt supply chains, planning, purchasing, scheduling, manufacturing and warehousing operations for many companies in the outdoor sports industry before becoming the CEO and President of two of them. In every case, we’ve been able to reduce inventory and increase fill rates by using numbers and formulas.

Now, not to oversimplify purchasing and inventory management because there are a number of variables which impact both, specifically demand, and we all know demand keeps changing. But, that is also the reason to use numbers and formulas so you don’t guess what to buy and store. For this article, I’m going to focus on classifying your inventory in A, B & C buckets and on service levels as those two drive the rest of the process and formulas.

A-B-C Inventory

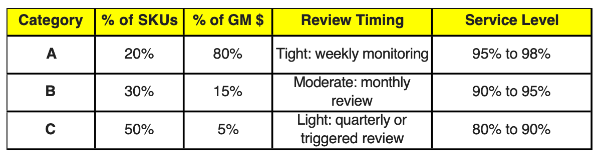

All items are not equal. Some generate a very high gross profit margin percentage and some generate high gross profit dollars. Ideally many do both. You should classify your inventory in A, B and C buckets so you can focus on your more important items, reduce inventory and increase profits. Your A items are most important followed by B then C. The graphic below shows a typical Pareto analysis in determining which items to categorize as A, B or C.

I’m surprised how many companies don’t implement this basic planning discipline as it helps tremendously with managing purchases and inventory. At one of the companies I was leading, the buyers were not using A, B, C classifications and therefore reviewing all SKUs every time they ran a planned order report. They spent a lot of wasted time ruling out those items they didn’t need to review and trying to identify the more important ones. When we implemented the A, B, C categories, they ran reports for only the A items weekly, the B items every two weeks and the C items monthly. It saved a lot of time and significantly improved the buying process.

Service Levels

Now that you’ve identified your A, B and C items, you now need to decide how often you want to have that item in stock when ordered. This is called the service level, and it typically ranges from 80% to 99%. The higher the service level, the higher the amount of inventory you have, some consider it safety stock, but that also increases your order fill rate, revenues and profits. Typically, your A items will have service levels in the 95% to 98% range, B’s in the 90% to 95% range and C’s in the 80% to 90%.

Ideally your ERP or MRP system has fields for these classifications, but I’ve found that many don’t. We’ve typically used offline tools to make these calculations but they have been well worth it. We’ll review and refresh the classifications and service levels maybe twice a year.

Summary

So let’s rerun the buying process again with these improvements. We’ll focus on the A items. It’s the beginning of the week and we run the “A Items to Purchase Report”. It first only reviews the A items. The computer looks at the current inventory quantity, average historical demand (might need an article on this also), delivery lead time, service level, economic order quantity (damn, maybe another article) and recommends how many to buy. You review the recommendations, make some changes based on the monthly sales forecast (yeah, I know you don’t have one…) then hit submit. You can run the “B items to Purchase Report” in the next week or two.

By categorizing your items and adding service levels, you’ll remove the guessing of what to buy, buy the correct amount, typically reducing inventory in your B and definitely C items but buying more of your A items which increases sales and profits. Easy!

We’ve all heard it: “The early bird gets the worm.” This adage holds true when it comes to planning for a successful week at the SHOT Show®. With the second half of 2026 already here, the 2027 SHOT Show is on the not-so-distant horizon. It’s never too early to develop a winning strategy for you and your team.

Your decision to attend the largest event in the firearm industry represents a sizable investment — and any way to enhance the value of your time in Las Vegas at The Venetian Expo and Caesars Forum is a worthy consideration. Locking in your hotel stay well in advance of the show represents one way to immediately add value.

Jimmy Hyman, vice president and general manager of Green Top Sporting Goods in Ashland, Va., has attended the past 12 SHOT Shows. As needs have changed over the years, he’s spearheaded accommodations for anywhere between three to 11 staff members. Whether it’s 11 or a smaller figure, a team’s flights, hotel rooms and meals for an entire week quickly add up.

By the conclusion of SHOT Week® each year, Hyman has already prepared for the next year’s show by booking his team’s accommodations.

“Before we leave Las Vegas, I make our reservations at The Venetian. Over the past 12 years we’ve stayed at Rio and Treasure Island. But, by sheer convenience, The Venetian can’t be beat. By booking a year out, we lock in a better rate,” he said.

Dual Benefits of Early Reservations

Booking accommodations early not only results in a more favorable rate, but also broad selection from the show’s headquarters hotel and any of the nearly 20 official SHOT Show hotels available through onPeak. Several of these hotels are easy walking distance (or directly connected) to The Venetian Expo and Caesars Forum — providing further convenience and savings for getting to and from the exhibition halls. (Rideshare, taxi, parking and rental car expenditures would be significantly reduced or not even needed.)

As of this writing, many of the official SHOT Show hotels have budget-friendly rates — available at a nightly rate of $250 or less. Over the course of four or more nights during SHOT Week, these economical prices make a real difference.

An additional benefit of securing hotel accommodations early is it provides an opportunity to lock in better airfare rates. All of this combines to provide further visibility of expected expenses before attending the SHOT Show, allowing for you to budget for extra incidentals.

As the early bird gets the worm, the early planner for the 2027 SHOT Show has more options and ability to secure vital savings. The 2027 SHOT Show will be here before we know it, running Jan. 19–22.

As always, an active NSSF membership will help you save at SHOT Show by providing special pricing on exhibit space, event registration, SHOT University™ educational sessions, Lead Retrieval and complimentary access to the NSSF member lounges around the show. Check your membership status today by contacting membership@nssf.org.